https://zenblis.com/glossary/va-aid-and-attendance

VA Aid and Attendance

Aid and Attendance is the VA pension enhancement that pays for senior care — in-home help, assisted living, memory care, or nursing home. Up to $3,845 per month in 2026 for qualifying wartime veterans and surviving spouses.

By Derek Belfield - 2026-04-26

Definition

VA Aid and Attendance is a tax-free enhanced pension benefit, paid monthly to qualifying wartime veterans and surviving spouses who need help with activities of daily living or are housebound, that can be used to pay for in-home care, assisted living, memory care, or nursing home costs.

Extended definition

VA Aid and Attendance is the most consequential federal payment source for senior care that families consistently overlook.

The official VA name for the underlying program is the Veterans Pension; Aid and Attendance is an enhancement layered on top of the basic pension when a veteran or surviving spouse needs ongoing personal care.

How it works

The benefit operates as a needs-based monthly cash payment. The VA sets a Maximum Annual Pension Rate (MAPR) ceiling for each household configuration, then subtracts the household's countable income — Social Security, pension, retirement payments, and similar sources — to calculate the actual monthly pension. Critically, unreimbursed medical expenses (including the cost of in-home care, assisted living, memory care, or nursing home care) reduce countable income, often dramatically. A Veteran spending $4,500 per month on assisted living can legitimately offset most or all of their income for VA purposes, which is what brings many otherwise-ineligible-looking applicants into qualification.

The actual monthly payment is the MAPR minus the household's countable income, so a Veteran with significant other income may receive less than the maximum. The 2026 net worth limit (combined assets and annual income, excluding the primary residence and basic personal items) is $163,699; applicants exceeding this limit are not eligible until they spend down or restructure assets.

Eligibility

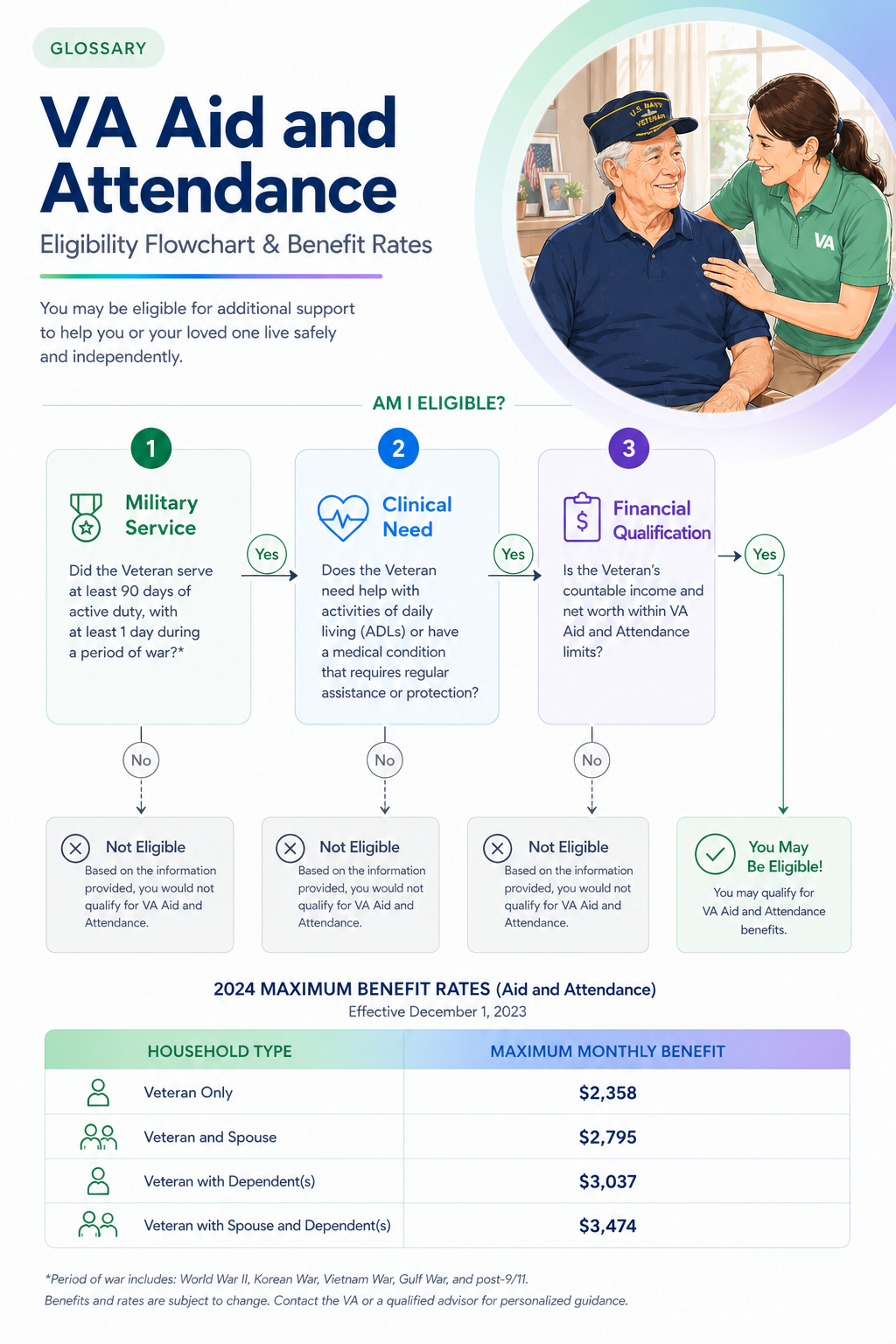

Eligibility requires three things:

military service,

clinical need, and;

financial qualification

Military service generally means at least 90 days of active duty with at least one day during a recognized wartime period (specific service requirements depend on enlistment date). Surviving spouses qualify based on the deceased veteran's service if they were married for at least one year before the veteran's death, or any length of time if they had a child together. Clinical need is established through VA Form 21-2680, completed by the applicant's physician, certifying that the veteran or spouse needs help with activities of daily living, is bedridden, is in a nursing home due to disability, or has profound visual impairment. Financial qualification involves the income and net worth tests above, with a three-year look-back period on asset transfers, established October 18, 2018, designed to prevent transfers solely to qualify.

The benefit is genuinely substantial — roughly 30 percent of the cost of an assisted living community, in some cases more — and is one of the few payment sources for senior care that does not require Medicaid spend-down. It can be used simultaneously as Medicaid in most cases, though receiving both reduces the VA pension. Aid and Attendance and the Housebound Benefit are mutually exclusive; Veterans can receive one or the other, not both, with Aid and Attendance offering the higher monthly amount.

Disability and Aid and Attendance

Disability compensation and Aid and Attendance are also generally mutually exclusive, with the VA paying whichever benefit is higher. Because applications are frequently denied for procedural rather than substantive reasons — incomplete forms, insufficient medical evidence, financial structuring that did not anticipate the look-back period — most families work with a VA-Accredited Claims Agent or attorney rather than applying alone.

Frequently Asked Questions

- Who qualifies for VA Aid and Attendance?

- Three thresholds must be met. Military service: typically at least 90 days of active duty with at least one day during a wartime period (surviving spouses qualify based on the veteran's service if married at least one year before death). Clinical need: needing help with activities of daily living, being bedridden, residing in a nursing home due to disability, or having profound visual impairment, certified by a physician on VA Form 21-2680. Financial qualification: net worth (combined assets and annual income, excluding primary residence and basic personal items) below $163,699 in 2026, and countable income within VA pension limits.

- How much does VA Aid and Attendance pay in 2026?

- For the December 1, 2025 through November 30, 2026 benefit year, maximum monthly Aid and Attendance amounts are: $2,358 for a single veteran with no dependents, $2,795 for a veteran with one dependent, $3,845 for two veterans married to each other where both qualify, and $1,515 for a surviving spouse with no dependents. Actual payments are the maximum minus the applicant's countable income. The benefit is tax-free and is paid in 12 equal monthly installments.

- What can VA Aid and Attendance be used for?

- The benefit is paid as a tax-free cash allowance that the recipient can use as they choose, but most use it to pay for long-term care services. Eligible uses include in-home care from agency caregivers or family members (with some restrictions), adult day services, assisted living community fees, memory care, and nursing home costs. The VA does not require receipts for how the money is spent — the application establishes that long-term care costs are creating the need, but the benefit itself is unrestricted cash.

- Can I receive VA Aid and Attendance and Medicaid at the same time?

- Yes, in most cases, though benefits may be reduced. Aid and Attendance is added on top of the basic VA pension, and the Aid and Attendance and Housebound enhancement portions do not count toward Medicaid's income limit. The basic pension portion may count toward Medicaid income depending on the state. A single nursing home Medicaid beneficiary's VA pension is typically reduced to $90 per month while the Medicaid benefit is active. Medicaid does require applicants to apply for any VA benefits they may be entitled to. Coordinating both benefits requires careful planning, often with an elder-law attorney or VA-Accredited Claims Agent.

- What is the VA Aid and Attendance look-back period?

- The VA implemented a three-year look-back period on asset transfers effective October 18, 2018. The VA reviews any assets given away or sold for less than fair market value during the three years before an Aid and Attendance application. Transfers that violate the look-back can trigger a penalty period of ineligibility. Note this is shorter than Medicaid's 60-month look-back. Families coordinating VA benefits and Medicaid eligibility should plan with both look-back periods in mind, ideally well before benefits are needed.

- What's the difference between Aid and Attendance and the Housebound Benefit?

- Both are pension enhancements added to the basic VA pension. Aid and Attendance is for veterans or surviving spouses who need regular help with activities of daily living, are bedridden, are in a nursing home, or have profound visual impairment. The Housebound Benefit is for veterans with a permanent disability that confines them substantially to their immediate home, typically a 100 percent disabling condition. A veteran can receive one or the other, not both. Aid and Attendance pays a higher monthly amount and is the more commonly used benefit for senior care.

- How do I apply for VA Aid and Attendance?

- The standard form is VA Form 21-2680 (Examination for Housebound Status or Permanent Need for Regular Aid and Attendance), completed by the applicant's physician, submitted with the basic pension application (VA Form 21P-527EZ for veterans or VA Form 21P-534EZ for surviving spouses) to the VA Pension Management Center or a VA regional office. Many applications are denied for procedural reasons such as incomplete documentation, financial structuring that didn't account for the look-back period, or insufficient medical evidence. Most families work with a VA-Accredited Claims Agent, an accredited Veterans Service Organization, or an elder-law attorney rather than applying alone.