https://zenblis.com/glossary/medicaid

Medicaid

Medicaid is the joint federal-state program that pays for what Medicare doesn't — long-term nursing home care, in-home personal care, and (in many states) some assisted living services. Eligibility rules vary by state and require both income and asset limits.

By Derek Belfield - 2026-04-26

Definition

Medicaid is a joint federal and state health insurance program for people with limited income and resources, and the largest single payer of long-term nursing home care in the United States — covering services Medicare does not, including custodial care for seniors who meet financial and clinical eligibility requirements.

Expanded definition

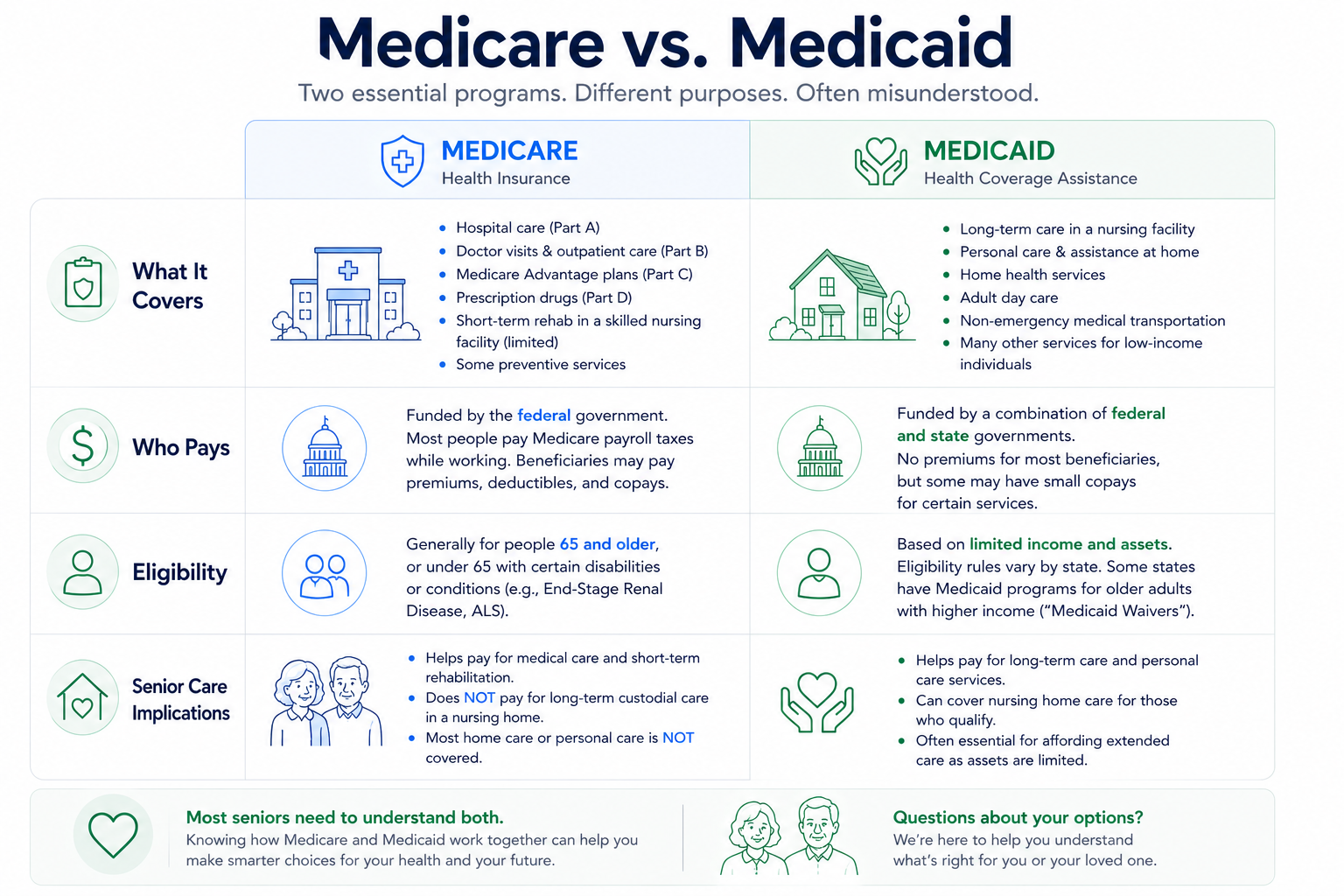

Medicaid was created in 1965 alongside Medicare under Title XIX of the Social Security Act, but it works differently in nearly every important way. Where Medicare is a federal program with uniform rules, Medicaid is jointly funded by the federal and state governments and administered by each state within federal parameters. This means eligibility rules, covered services, and even the program's name change at the state line — Medi-Cal in California, MassHealth in Massachusetts, TennCare in Tennessee. For families navigating senior care, the most consequential thing about Medicaid is what it covers that Medicare does not: long-term custodial care, including most nursing home stays.

Medicaid is the single largest payer of long-term nursing home care in the United States, covering more than 60 percent of nursing home residents nationally. To qualify for long-term care Medicaid, a senior must meet two thresholds:

a financial test (income and asset limits) and;

a functional test (typically requiring a "Nursing Home Level of Care" determination based on activities of daily living and cognitive status).

For married couples

For married couples, federal "spousal impoverishment" protections preserve a share of the couple's resources for the spouse who continues to live in the community. In 2026, the Community Spouse Resource Allowance lets a community spouse retain up to $162,660 in assets, plus a Monthly Maintenance Needs Allowance of up to $4,066.50 in income — figures designed to prevent the at-home spouse from becoming impoverished while their partner is in a nursing home. These rules are a significant focus of elder-law planning, and a Certified Elder Law Attorney can help families understand options like Medicaid Compliant Annuities, Miller Trusts (used in "income cap" states), and the rules around the 60-month look-back period that scrutinizes asset transfers.

Additional coverage

Beyond nursing home coverage, Medicaid pays for a wide range of services Medicare does not — including personal care, adult day services, home modifications, and respite for family caregivers. Most of these are delivered through Home and Community Based Services (HCBS) Waivers, which operate as separate programs in each state with their own waiting lists. In some states, Medicaid will also cover assisted living services through HCBS waivers, though it does not pay for room and board in those settings. Because Medicaid is the safety net for long-term care, it is also the program most often involved when families face the financial reality that Medicare's coverage has ended. Applying takes an average of six months from start to approval, which is one reason elder-law attorneys consistently advise families to plan early — well before a crisis forces the issue.

Frequently Asked Questions

- What's the difference between Medicare and Medicaid?

- Medicare is federal health insurance for people 65 and older (and certain younger people with disabilities), funded by payroll taxes and available regardless of income. It covers hospital and medical care but not long-term custodial care. Medicaid is a joint federal-state program for people with limited income and resources, and is the largest payer of long-term nursing home care nationally. Many seniors are "dual-eligible," qualifying for both — Medicare covers their medical care, Medicaid covers their long-term care and helps with Medicare premiums and copays.

- What does Medicaid cover that Medicare does not?

- Medicaid covers long-term custodial nursing home care, in-home personal care, adult day services, home modifications, respite care for family caregivers, and (in many states through HCBS waivers) some assisted living services. Medicare does not cover any of these when they are the primary care need. Medicaid also helps low-income Medicare beneficiaries pay their Medicare premiums, deductibles, and copays through Medicare Savings Programs.

- What are the income and asset limits for long-term care Medicaid?

- In most states in 2026, the income limit for long-term care Medicaid is $2,982 per month for a single applicant, based on 300 percent of the federal Supplemental Security Income benefit rate. The asset limit is typically $2,000 for an individual, though some states permit higher amounts — California allows up to $130,000, for example. A primary home is generally exempt if the applicant's spouse, minor child, or disabled child lives there, or if home equity falls below the state's limit. Income and asset rules differ for married couples and for HCBS waiver applicants, and limits change annually.

- What is the Medicaid look-back period?

- The Medicaid look-back period is a 60-month window before the date of a long-term care Medicaid application during which the state reviews any asset transfers. Assets given away or sold for less than fair market value during this period can trigger a penalty period of Medicaid ineligibility. The penalty length is calculated by dividing the transferred amount by the state's average monthly nursing home cost. The look-back period is one of the main reasons elder-law attorneys advise families to start planning years before Medicaid is needed — last-minute transfers almost always trigger penalties.

- Does Medicaid cover assisted living?

- It depends on the state. Medicaid does not pay for room and board in any assisted living community. However, in many states, Medicaid covers personal care services delivered inside an assisted living community through Home and Community Based Services (HCBS) waivers. The combination — Medicaid paying for clinical care services while the family or another source covers room and board — is how Medicaid-funded assisted living typically works. Coverage details vary widely by state and by waiver, and most HCBS waivers have enrollment caps and waiting lists.

- What is a "spend-down" and how does it work?

- Spend-down refers to the process of reducing assets to qualify for long-term care Medicaid. Because most states require an applicant to have $2,000 or less in countable assets, families often spend savings on care, home modifications, prepaid funeral arrangements, or other allowed expenses to meet the threshold. Some states also have "medically needy" programs that allow applicants to spend down income on medical bills to qualify. Spend-down is heavily regulated and the rules vary by state, which is why elder-law planning before applying is consistently advised — done correctly, it preserves more for the family; done incorrectly, it can trigger look-back penalties.

- What does it mean to be "dual-eligible"?

- Dual-eligible refers to seniors who qualify for both Medicare and Medicaid. There are roughly 12 million dual-eligible Americans. Medicare covers their hospital and medical care; Medicaid covers their long-term care, helps pay Medicare premiums and copays, and may cover services Medicare does not. Special Needs Plans (D-SNPs) are Medicare Advantage plans designed specifically for dual-eligibles and often coordinate the two programs more tightly than separate enrollment in each.