https://zenblis.com/glossary/medicare

Medicare

Medicare is federal health insurance, not long-term care insurance. It covers hospitals, doctors, short-term skilled nursing, and prescription drugs — but not assisted living, memory care, or most nursing home stays.

By Derek Belfield - 2026-04-26

Definition

Medicare is the federal health insurance program for Americans aged 65 and older, plus certain younger people with disabilities or end-stage renal disease, organized into four parts (A, B, C, and D) that together cover hospital stays, outpatient medical services, prescription drugs, and most short-term post-acute care — but not long-term custodial care.

Expanded definition

Medicare was created in 1965 under Title XVIII of the Social Security Act and today covers more than 65 million Americans. It is administered by the Centers for Medicare and Medicaid Services (CMS). For families navigating senior care, the program's most important characteristic is also the most misunderstood: Medicare is health insurance, not long-term care insurance. It covers medically necessary hospital and outpatient care, but it does not pay for the day-to-day personal care that most seniors eventually need — the bathing, dressing, medication management, and supervision that defines assisted living, memory care, and most nursing home stays.

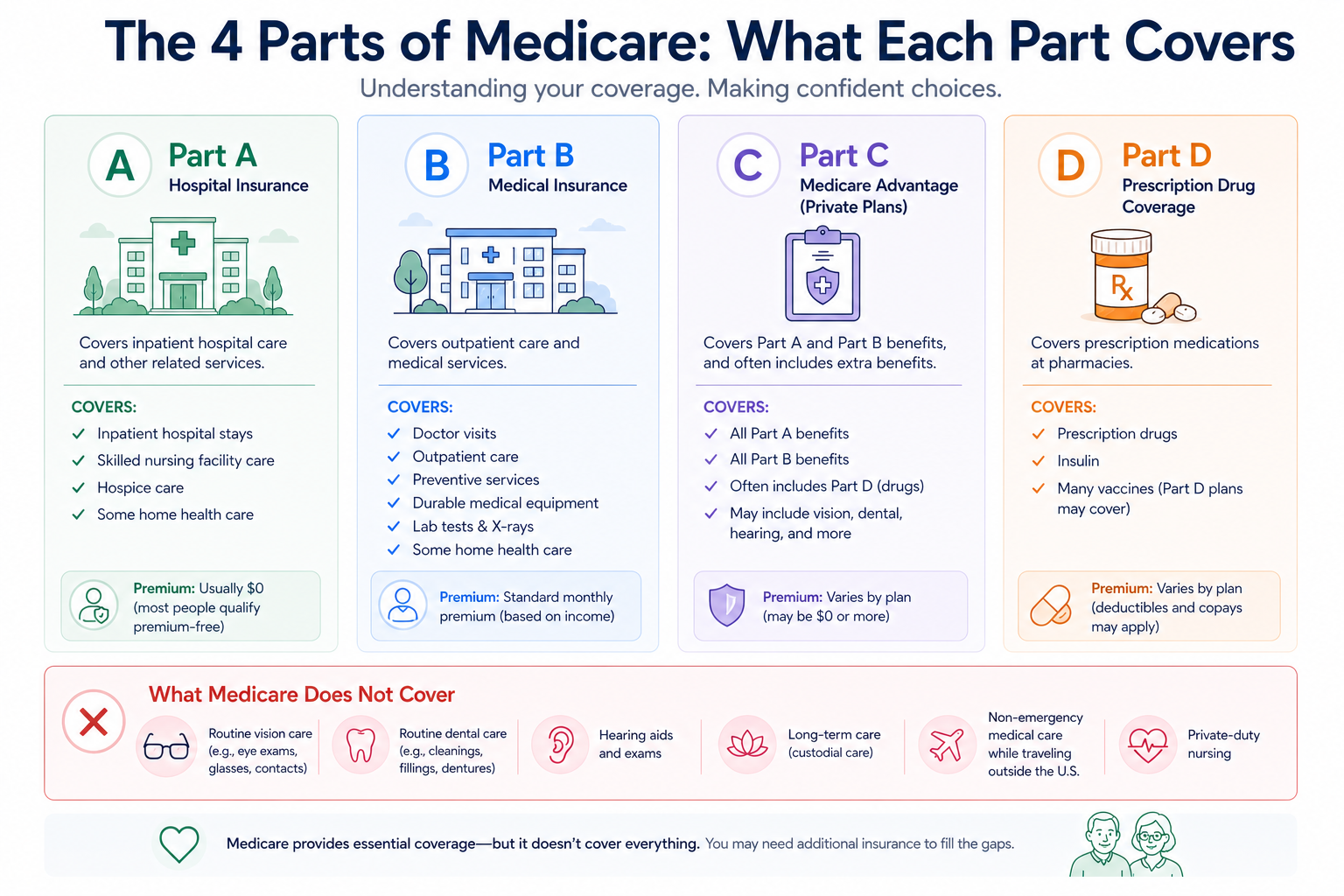

Original Medicare consists of two parts:

Part A (Hospital Insurance) covers inpatient hospital stays, short-term skilled nursing facility care after a qualifying hospitalization, hospice care, and some home health services. Most people pay no premium for Part A because they or a spouse paid Medicare payroll taxes for at least 40 quarters (10 years). The 2026 Part A inpatient deductible is $1,736 per benefit period.

Part B (Medical Insurance) covers physician visits, outpatient procedures, durable medical equipment, preventive care, and certain home health services. The standard Part B monthly premium in 2026 is $202.90, with an annual deductible of $283 and 20 percent coinsurance for most covered services after the deductible is met.

Two more parts add coverage options:

Part C, also called Medicare Advantage, is private insurance that bundles Parts A and B (and usually D) into a single plan offered by a Medicare-approved company. Most Medicare Advantage plans include extra benefits Original Medicare does not — vision, dental, hearing, fitness — but they also use provider networks and prior-authorization rules that Original Medicare does not.

Part D is prescription drug coverage, sold separately as a stand-alone Prescription Drug Plan or bundled into a Medicare Advantage plan. The maximum 2026 Part D deductible is $615, and a new annual out-of-pocket cap of $2,100 means once a beneficiary reaches that threshold, they pay nothing more for covered drugs that year.

What Medicare doesn't cover

For senior care decisions, the critical point is what Medicare does not cover. Medicare does not pay for room and board in assisted living, memory care, or long-term nursing home stays. It does not pay for non-medical home care — help with bathing, dressing, meal preparation, or companionship — when that is the only care a person needs.

It covers up to 100 days per benefit period of skilled nursing facility care after a qualifying three-day inpatient hospital stay (with a $217 daily copay for days 21–100 in 2026), but only as long as the patient continues to make measurable improvement. Once recovery plateaus, Medicare coverage ends, often with only 48 hours' notice. Most families discover this gap precisely when they most need help understanding it. Medicaid, long-term care insurance, the VA Aid and Attendance benefit, and private savings are the primary sources that fill the gap Medicare leaves behind.

Frequently Asked Questions

- What are the four parts of Medicare?

- Part A covers inpatient hospital stays, short-term skilled nursing care, hospice, and some home health services. Part B covers outpatient medical care, physician visits, and durable medical equipment. Part C, also called Medicare Advantage, is private insurance that bundles A, B, and usually D into one plan. Part D is prescription drug coverage. Original Medicare refers to Parts A and B together; Part C is an alternative way to receive A and B benefits through a private plan.

- Does Medicare pay for assisted living or memory care?

- No. Medicare does not pay for room and board in assisted living, memory care, or long-term nursing home stays because those settings provide custodial care, not medical care. Medicare may cover specific medical services delivered to a senior inside one of those settings — physician visits, hospice services, durable medical equipment — but not the residence itself. Most families pay assisted living and memory care costs through private savings, long-term care insurance, the VA Aid and Attendance benefit, or Medicaid HCBS waivers in states that cover those services.

- How much does Medicare cost in 2026?

- Most beneficiaries pay no premium for Part A. The standard Part B monthly premium in 2026 is $202.90, with a $283 annual deductible and 20 percent coinsurance after that. The Part A inpatient hospital deductible is $1,736 per benefit period. Part D premiums vary by plan, with an average of $34.50 per month in 2026 and a maximum deductible of $615. Higher-income beneficiaries pay additional surcharges through the Income-Related Monthly Adjustment Amount (IRMAA), which can raise Part B premiums to as much as $689.90 per month in 2026.

- What is the difference between Original Medicare and Medicare Advantage?

- Original Medicare is the traditional federal program — Parts A and B — that lets beneficiaries see any provider who accepts Medicare nationwide, with no networks or prior-authorization for most services. Medicare Advantage (Part C) is private insurance that bundles A and B (and usually D) into one plan with extra benefits like dental and vision, but uses provider networks and may require prior authorization. Roughly half of Medicare beneficiaries are enrolled in Medicare Advantage. Each option has trade-offs in cost, flexibility, and out-of-pocket exposure that depend on a senior's health, location, and preferred providers.

- What does Medicare cover for skilled nursing facility care?

- Medicare Part A covers up to 100 days per benefit period of skilled nursing facility care, but only if the patient had a qualifying inpatient hospital stay of at least three consecutive days, is admitted to the SNF within 30 days of discharge, and continues to need skilled care. The first 20 days are covered in full; days 21–100 require a daily copay of $217 in 2026; Medicare pays nothing after day 100. Coverage ends when the patient stops making measurable improvement, even if it's before day 100 — a transition that catches many families unprepared.

- What is IRMAA and who pays it?

- IRMAA stands for Income-Related Monthly Adjustment Amount — a surcharge added to Medicare Part B and Part D premiums for higher-income beneficiaries. CMS uses Modified Adjusted Gross Income (MAGI) from two years earlier to determine whether a surcharge applies. About 8 percent of Medicare beneficiaries pay IRMAA. In 2026, IRMAA raises Part B premiums from $284.10 to $689.90 per month depending on income, with the highest rate applying to individuals with incomes above $500,000 (or $750,000 for married couples).