https://zenblis.com/glossary/power-of-attorney

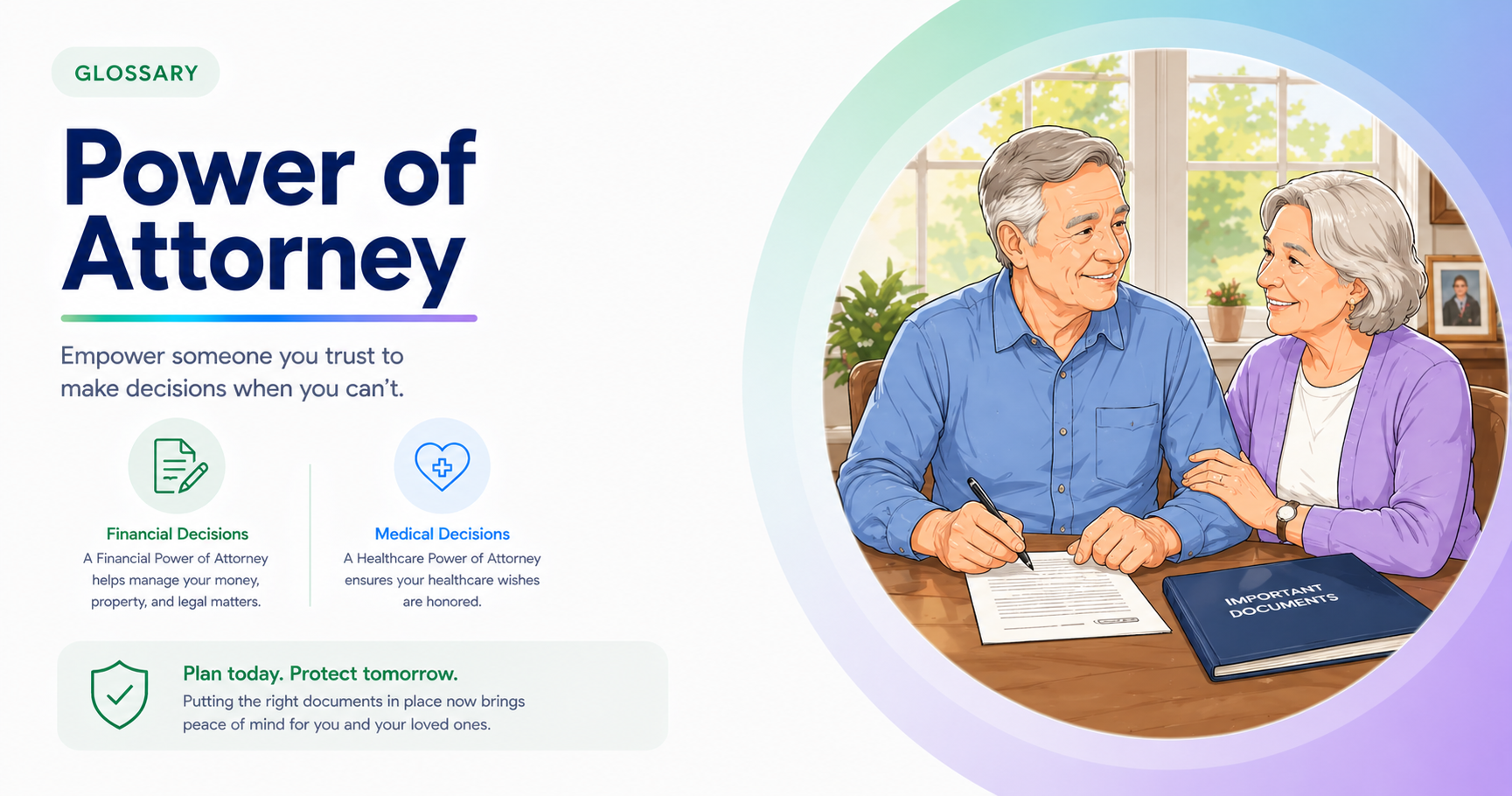

Power of Attorney (POA)

A Power of Attorney is one of the most important legal documents in senior care — and one of the most often delayed. Most families need two: a financial POA and a healthcare POA, both made durable, both established while the senior still has capacity.

By Derek Belfield - 2026-04-27

Definition

A Power of Attorney (POA) is a legal document in which one person — the principal — authorizes another person — the agent or attorney-in-fact — to act on their behalf, with senior care planning typically requiring two separate documents: a financial POA covering money matters and a healthcare POA covering medical decisions.

Expanded definition

A Power of Attorney is one of the most consequential legal documents in senior care planning, and one of the most consistently put off until it's too late. The document grants legal authority — the principal authorizes someone else (called an agent or attorney-in-fact, even if that person isn't a lawyer) to act in their place. Without one, families confronting a parent's sudden hospitalization or cognitive decline often discover that no one has the legal authority to pay bills, sign care contracts, or make medical decisions, and the only option is petitioning a court for guardianship or conservatorship — a lengthy, expensive, and emotionally exhausting process that strips the senior of legal autonomy.

Distinctions

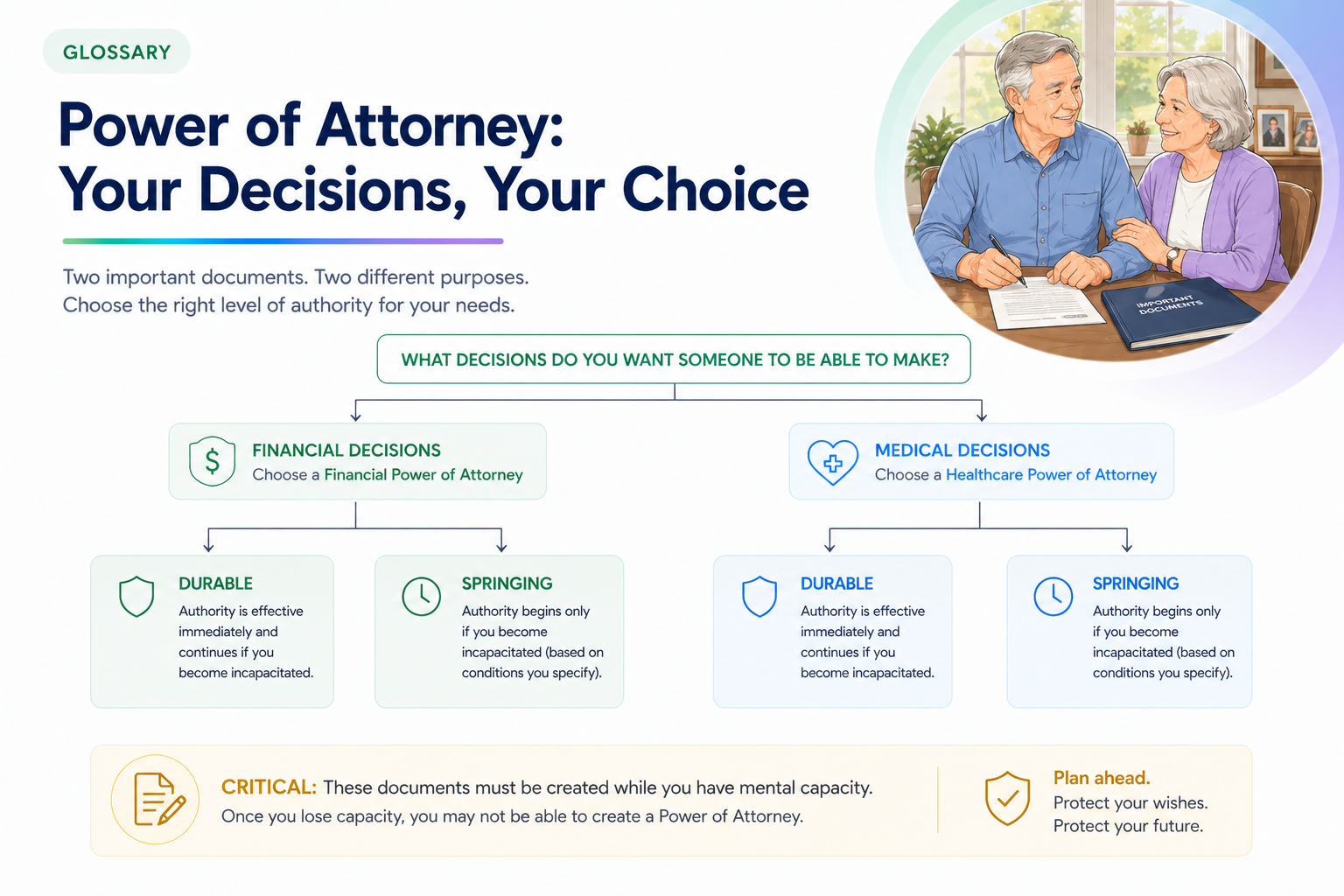

Three distinctions matter for senior care families:

First, a POA must be established while the principal still has capacity to understand the document. Once a senior loses decision-making capacity to dementia, stroke, or other cognitive change, it is too late to create a POA.

Second, the document must be "durable" to remain valid through incapacity. A non-durable POA automatically ends if the principal becomes mentally incapacitated — the opposite of what most senior care families need. Most states presume durability unless the document specifies otherwise, but wording matters and varies by state.

Third, financial decisions and healthcare decisions are governed by separate documents in most states, even when the same agent is named for both. Combining them into one document is generally not legally effective.

Financial POAs

Financial POAs grant authority over money, property, and legal matters — paying bills, managing investments, filing tax returns, signing contracts, selling or buying real estate, accessing bank accounts, applying for benefits like Medicaid or VA pensions. The scope can be broad (general POA covering all financial decisions) or narrow (limited POA covering only specific transactions like one real estate closing). Some financial POAs are "springing" — taking effect only after a physician certifies that the principal is incapacitated — while others take effect immediately when signed. Springing POAs sound safer but often cause practical problems because banks and institutions can be reluctant to honor them without clear evidence of incapacity.

Healthcare POAs

Healthcare POAs go by many names depending on state — Medical Power of Attorney, Healthcare Proxy, Durable Power of Attorney for Health Care, Advance Healthcare Directive, Patient Advocate Designation. They authorize the named agent to make medical decisions if the principal cannot, including consenting to or refusing treatment, choosing care settings (hospital, nursing home, hospice), reviewing medical records under HIPAA, and discussing treatment with physicians. Healthcare POAs typically only become effective when the principal loses capacity, and the agent must follow the principal's known wishes. Many states combine the healthcare POA with a Living Will into a single Advance Directive document. Healthcare POAs are the legal foundation for the family conversations that hospice referrals, memory care decisions, and end-of-life planning all depend on.

Practical realities

A few practical realities worth understanding. POAs are recognized across state lines but state-specific forms are usually preferred — a parent who moves from Florida to Texas should update both POAs to use Texas-specific forms. Banks and institutions sometimes refuse to honor older POAs or insist on their own internal forms; this is a common point of friction families discover only when they try to use the document. Naming co-agents who must agree creates protection but also potential gridlock; most attorneys recommend naming a primary agent and a backup. POAs end at death — they do not authorize the agent to handle estate matters, which is the role of an executor named in a will. And finally, POA can be revoked at any time by a competent principal, simply by signing a written revocation and notifying the agent, financial institutions, and healthcare providers. For families, working with a Certified Elder Law Attorney to prepare or update POAs alongside a Living Will, HIPAA authorization, and (depending on the situation) a trust is the standard approach.

Frequently Asked Questions

- What's the difference between a financial POA and a healthcare POA?

- A financial POA authorizes the agent to handle money, property, and legal matters — paying bills, managing investments, signing contracts, applying for benefits, buying or selling real estate. A healthcare POA authorizes the agent to make medical decisions, choose care settings, review medical records, and consent to or refuse treatment. In most states, these are two separate documents. Many people name the same person as agent for both, but they don't have to — it's reasonable to name a financially capable child for the financial POA and a different family member for the healthcare POA if circumstances suggest different strengths.

- What does "durable" mean in a Power of Attorney?

- Durable means the POA remains valid even after the principal becomes mentally incapacitated. A non-durable POA automatically ends when the principal loses capacity — the opposite of what families need for senior care planning. Most states now presume durability unless the document explicitly says otherwise, but precise wording varies by state. The senior care use case essentially always requires a durable POA for both financial and healthcare matters.

- What happens if a senior loses capacity without a Power of Attorney?

- Family members typically have to petition a court to be appointed as guardian (for healthcare and personal decisions) or conservator (for financial decisions). The terminology varies by state — some states use "guardian" for both, others use different titles. The process is public, expensive (often several thousand dollars), can take months, and strips the senior of significant legal autonomy. The court selects who serves, which may not match the family's preference. Establishing POAs in advance avoids this entirely, which is why elder-law attorneys consistently advise families to address POA documents long before they're needed.

- Can I create a Power of Attorney for my parent who already has dementia?

- It depends on whether the parent still has decision-making capacity to understand the document. Capacity is not all-or-nothing — a parent in early-stage dementia may still have legal capacity to sign a POA, while a parent in middle or late stages typically does not. Capacity is assessed in the moment, and a parent who has good days and bad days may sign on a clear day with proper safeguards. An elder-law attorney can evaluate whether capacity exists and document it appropriately. If capacity has been lost, the only path forward is petitioning the court for guardianship or conservatorship.

- Is a Power of Attorney recognized in every state?

- A POA validly executed in one state must generally be honored in every state, but practical complications arise. Banks and other institutions often prefer or require their own state-specific forms. Real estate transactions typically require a POA that complies with the local state's recording rules. Many elder-law attorneys recommend updating POAs when a senior moves to a new state, both to reduce friction and to ensure the document reflects current state law. POAs covering property in multiple states should be reviewed by an attorney familiar with each state's rules.

- When does a healthcare Power of Attorney take effect?

- A healthcare POA typically takes effect only when the principal loses capacity to make their own medical decisions — the agent does not have authority to override decisions while the principal can still make them. As long as the principal has capacity, they direct their own care, even if the agent disagrees. The agent's authority is a safety net, not a substitute. Some healthcare POAs include specific guidance on when authority activates (for example, after two physicians certify incapacity); others rely on the attending physician's judgment.

- Can a Power of Attorney be revoked?

- Yes, at any time, as long as the principal has decision-making capacity. Revocation typically requires a written, signed statement notifying the agent, all financial institutions, healthcare providers, and anyone holding a copy of the original document. Destroying all copies of the original POA helps but is not legally sufficient — the written revocation creates the legal record. After revocation, the principal can create a new POA naming a different agent. Revocation does not require an attorney, though documenting the revocation properly is important for institutions to honor it.